10-Year Treasury Yield

Source: Bloomberg

First, some basic facts:

The Treasury issued $1.7 trillion of securities on a net basis (meaning that total issuance exceeded the amount of securities maturing by that amount) in fiscal year 2009 and expects to borrow a net of $1.5 to $2.0 trillion in the current fiscal year, as the cumulative amount of budget deficits over the next three fiscal years is estimated to be in the area of $3.5 trillion. By all standards, these are staggering numbers.

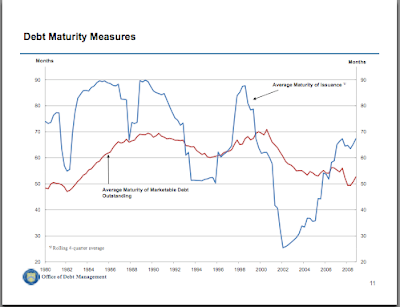

Since the beginning of the decade, the average maturity of the Treasury's outstanding debt has dropped from about 70 months to approximately 50 months recently, as a result of appreciably heavier reliance on short-term debt issuance over medium- and longer-term maturities for most of that period. The most recent such level represents the lowest since the early '80s.

In announcing that decision, in the context of the quarterly press conference unveiling its broader financing plans, the Treasury went at great lengths to emphasize that the project of lengthening the average maturity of its debt would be implemented very gradually to avoid disrupting market expectations and breaking abruptly with past patterns. Still, a target of reaching an average of 60 months in fiscal 2010 was stated, with an eye on extending it to 84 months over the medium-term, which would represent a historical high.

The Treasury's decision to extend the average maturity of its debt is a sound one, not only on the grounds of prudent borrowing management by spreading out its debt burden over a longer horizon but also on the count of reducing its borrowing costs over time. The latter rationale has generally been a sensitive issue for the Treasury over the years, as it has always maintained that it is not in the business of attempting to "time the market" by adopting views on the future direction of interest rates- an overall sensible approach for a government.

Still, taking advantage, in a measured way, of the unusually low levels of long-term yields (courtesy of a severe financial crisis and associated economic recession) to implement a solid debt management principle of better balancing the ratio of short- to long-term outstanding debt makes perfect sense. Inasmuch as the Treasury wants, understandably, to stay clear of the hazardous enterprise of predicting interest rates, ignoring completely a historical opportunity that would allow it to materially reduce its interest costs on a mushrooming debt over the medium-term would be almost tantamount to malpractice.

Anthony Karydakis

In announcing that decision, in the context of the quarterly press conference unveiling its broader financing plans, the Treasury went at great lengths to emphasize that the project of lengthening the average maturity of its debt would be implemented very gradually to avoid disrupting market expectations and breaking abruptly with past patterns. Still, a target of reaching an average of 60 months in fiscal 2010 was stated, with an eye on extending it to 84 months over the medium-term, which would represent a historical high.

The Treasury's decision to extend the average maturity of its debt is a sound one, not only on the grounds of prudent borrowing management by spreading out its debt burden over a longer horizon but also on the count of reducing its borrowing costs over time. The latter rationale has generally been a sensitive issue for the Treasury over the years, as it has always maintained that it is not in the business of attempting to "time the market" by adopting views on the future direction of interest rates- an overall sensible approach for a government.

Still, taking advantage, in a measured way, of the unusually low levels of long-term yields (courtesy of a severe financial crisis and associated economic recession) to implement a solid debt management principle of better balancing the ratio of short- to long-term outstanding debt makes perfect sense. Inasmuch as the Treasury wants, understandably, to stay clear of the hazardous enterprise of predicting interest rates, ignoring completely a historical opportunity that would allow it to materially reduce its interest costs on a mushrooming debt over the medium-term would be almost tantamount to malpractice.

Anthony Karydakis

No comments:

Post a Comment