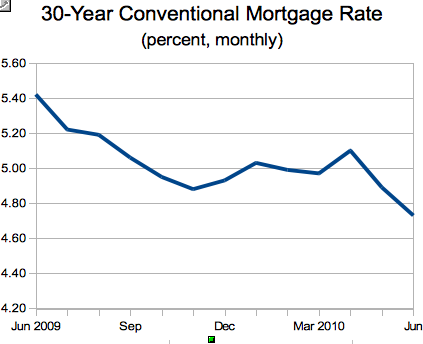

Although, in classic market modus operandi, the sheer anticipation of that outcome was enough to cause a modest back up in yields prior to the expiration of the Fed's program at the end of March, the reality is that mortgage rates have declined appreciably since the beginning of the year, with the 30-year fixed rate mortgage dipping to 4.67% last week, according to this morning's data released by the Mortgage Business Association (http://www.mortgagebankers.org/NewsandMedia/PressCenter/73294.htm).

Source: Federal reserve Bank of St. Louis, MBA

The fiscal turmoil in the eurozone since the beginning of the year, an ongoing downward drift of domestic inflation, and a modest loss of momentum in the economic reports recently have all conspired to fuel a powerful rally in the bond market, driving mortgage yields lower as well. This dynamic has trampled any demand/supply-related considerations stemming from the Fed's withdrawal from the mortgage market in the second quarter.

As we have argued before, supply is a temptingly convenient factor to use in any rationale attempting to forecast the direction of long-term yields. In reality, though, it has a particularly poor track record to justify such attention. The most dramatic perhaps demonstration of the exaggerated importance that markets often attribute to supply is the fact that Treasury yields have been able to absorb a massive onslaught of supply in the last 18 months, without any signs of indigestion and remain near historically record-low levels, despite an economic recovery that has been taking hold for nearly a year now.

The advocates of supply as a key determinant of market yields always offer the caveat of "all other things being equal". The problem is that, outside the universe of academic research and computer models, those "other things" are almost never equal. In fact, changes in supply conditions typically contain the very seeds of a powerful counter-effect that neutralizes its impact. For example, the massive Treasury fiscal deficits were the direct result of a sever financial crisis and deep recession, both of which were potent forces pushing yields lower.

A similar explanation accounts for the impressive resilience of mortgage rates following the end of the Fed's purchase program; that is, the broader conditions in both the domestic economy and global market environment were a far more dominant driving force of such yields than the end of the Fed's purchase program.

Anthony Karydakis