The moderate rise of long-term Treasury yields since late November seems to have already triggered a flurry of stories in the financial press as to its underlying reasons as well as to whether it represents the first stage of a sustained, cyclical, uptrend in such yields.

As attempts at explaining this development have been pouring in, the most commonly offered explanations offered in recent days for the back-up in 10-year Treasury yields by about 60 basis points to the 3.80-3.90% range during that period are mostly zeroing in on the following factors: 1) The prospect that the economic recovery underway may ignite inflationary pressures down the road, 2) The massive budget deficits projected over the next couple of years, in conjunction with the Treasury's expressly stated plan to shift its new issuance toward longer maturities may ultimately cause the market to choke on supply, 3) The easing of the previous anxiety in global financial markets has led to a an increasing gravitation of foreign investors toward emerging markets, therefore abandoning U.S. Treasuries, which in the midst of the financial storm of the last 1 1/2 year had largely played the traditional role of a safe-haven.

Viewed separately, none of the above factors offer a credible explanation as to the timing of the latest sell off in the Treasury market.

First, on the count of inflation fears creeping back into the Treasury market. Hard to believe that such fears are indeed real. The latest round of inflation numbers have been, if anything, reassuring regarding the price picture. Core CPI was flat in November, having averaged 0.1% in the last two months, wage pressures remain non-existent, the labor market slack is at its highest and, by most indications, inflation (given that it is a famously lagging economic indicator) is widely expected to drift somewhat lower over the next 12 to 18 months, even as the economic recovery is taking hold. Moreover, the Fed is already openly, and methodically, positioning itself to start addressing the anxiety-generating issue of its "exit strategy", adopting a posture that can only be assumed to have a soothing effect on the market. To argue that, somehow, against this decidedly benign price backdrop, the Treasury market was abruptly invaded by intense inflation concerns, defies basic facts and stretches any sense of logic.

Second, in regards to the the presumed supply concerns and dismal budget deficit prospects. Sure, but this is nothing new that was suddenly revealed to market participants at the end of November. Forecasts of massive fiscal deficits have been around for nearly a year now and have not become particularly gloomier of late. Moreover, the end of the Fed's program to purchase $300 billion of Treasury securities (which was clearly viewed as a factor supporting the market) had already ended at the end of September (so, nothing new really) and the Treasury had already announced on November 4th its intention to increase its issuance of long-term debt without any immediate adverse reaction visible at the time. In other words, it does not appear that anything new broke on the supply front around the turn of the month that would justify a fairly substantial back-up in long-tern yields.

Third, the story about a steady increase in global investors' risk appetite-resulting into a massive influx of capital in emerging market economies is hardly a new one; it has been a dominant theme for several months now, with only a" manageable", and rather transient, adverse effect on Treasury yields previously.

Perhaps a better framework for interpreting the latest back-up in yields would require a more practical, down-to-earth, approach that takes into account some simple realities as to how markets function, and which often get brushed aside to make room for more rational-sounding "explanations".

To start with, the latest rise in long-term yields, both in terms of the magnitude of the increase and also the absolute levels reached, was nothing particularly unusual to justify the emergence of any new anxiety about the direction of rates. In fact, 10-year yields touched 4% in June- having risen by 150 basis points since early spring- only to drop again to below 3 1/4% by October. The transparent, and understandable, reason for the much sharper back-up earlier in the year was the realization that the economy was about to emerge from the recession and previous assumptions about the potential deflation risk were quickly downgraded. The subsequent realization that the economic recovery was likely to be of the moderate kind, by historical standards, allowed to a pullback in yields by fall.

What is often missing from attempts to explain the Treasury market's every twist and turn is the very realization that markets are notoriously emotional entities. As such, they often have mood swings that can be triggered by any set of factors, which may have been lurking in the background fairly innocuously for a while suddenly come to the forefront, becoming every one's favorite "reason" for a certain price action. While none of the three "explanations" discussed above in this article make sense in isolation, all put together form the semblance of a rational backdrop against which the latest rise in yields can be viewed. It is also crucial to recognize that the latest sell off took place in the midst of mostly thin, holiday trading, undermining its true significance further.

To be sure, with the economy switching into a solid growth pattern ahead and the Fed on standby to start reversing the exceptionally easy monetary policy at some point over the next six to twelve months, Treasury yields are likely to move on balance somewhat higher in 2010. This would be hardly a ground-breaking development worth endless stories with purported "in-depth" explanations as to its underlying reasons. After all, that is what almost always yields do when the business cycle turns. That rise may be quite a circuitous affair. In fact, when the timing of Fed tightening is viewed as within reach, markets, in true form, are likely to overreact and yields may initially rise violently in the context of a flattening yield curve, while such an overreaction may be subsequently tempered by the realization that inflation is likely to remain firmly under control with the Fed in a highly vigilant posture.

But over-analyzing a fairly "run-of-the-mill" rise in Treasury yields over the last several weeks is probably a case of much ado about nothing...

Anthony Karydakis

Tuesday, December 29, 2009

Monday, December 28, 2009

A Holiday Gift from The Treasury

By Scott Tolep

On Christmas Eve, the US Treasury announced that it would provide unlimited capital over the next three years, if necessary, to cover losses suffered by mortgage agencies Fannie Mae and Freddie Mac (previously the limit was set at $200 billion each). The obvious initial reaction here is that the Treasury is issuing a “blank check” to the mortgage agencies and is jeopardizing the future direction and size of the ever-growing public debt. However, there are four compelling reasons to believe that the Treasury’s decision will not increase the public debt and will support the continued stabilization of the housing market and economy:

(1) After December 31, 2009, The Treasury will discontinue its purchases of MBS, which have totaled around $200 billion since the onset of the housing crisis and have kept mortgage rates at historical lows (The Fed has a separate MBS purchase program, set to expire at the end of first quarter 2010, and is expected to reach $1.25 trillion). The Treasury’s and Fed’s purchases have undoubtedly played key roles in keeping mortgage rates low and dramatically improving the housing market. As of October, unsold inventory of both new and existing homes were at their lowest levels in 3 years or more. It appears that the worst of the housing crisis is over, so it is likely that the agencies have already received the bulk of Treasury capital infusions they'll need (~$110 billion).

(2) Psychology plays an important factor in all markets, and the housing market is no exception. Yes, housing and the economy are stabilizing, but this painful cycle is still fresh in the minds (and bank accounts) of investors and lenders. The US will continue to experience periodic setbacks on the heels of this housing-led recession. With the Treasury discontinuing its MBS purchases, market participants are more likely to overreact to these setbacks, with the potential for destabilizing the housing market and economy and sending them back into a tailspin. The Treasury's decision to provide unlimited capital guarantees to the agencies over the next 3 years mitigates this risk.(3) The Treasury has gained significant credibility after recovering a large percentage of the TARP funds it had injected into the banking system. It was announced earlier this month that $185 of the $245 billion that TARP invested in banks (75% of total) is scheduled to be returned to taxpayers with a profit.

http://news.yahoo.com/s/nm/20091215/bs_nm/us_usa_bailout_treasury.(4) The Treasury’s decision should not lead to a loss of market discipline or create a “too-big-to-fail” attitude within the Agencies, as they are both currently under government control and underwriting standards are much tougher than they were in the 2005-2007 era.

Tuesday, December 22, 2009

Taking Advantage of the Low Yields

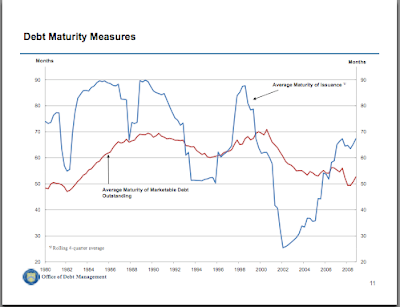

The Treasury announced last month that, moving forward, it intends to rely more heavily on the issuance of long-term coupon securities to finance its large budget deficits that are projected over the medium-term. While the Treasury's rationale for that shift was ostensibly to gradually lengthen the average maturity of its debt to levels more consistent with past trends, the unmistakable undercurrent of that decision was that the Treasury is also interested in taking advantage of the historically low levels of long-term yields for purposes of reducing its borrowing costs.

10-Year Treasury Yield

10-Year Treasury Yield

Source: Bloomberg

First, some basic facts:

The Treasury issued $1.7 trillion of securities on a net basis (meaning that total issuance exceeded the amount of securities maturing by that amount) in fiscal year 2009 and expects to borrow a net of $1.5 to $2.0 trillion in the current fiscal year, as the cumulative amount of budget deficits over the next three fiscal years is estimated to be in the area of $3.5 trillion. By all standards, these are staggering numbers.

Since the beginning of the decade, the average maturity of the Treasury's outstanding debt has dropped from about 70 months to approximately 50 months recently, as a result of appreciably heavier reliance on short-term debt issuance over medium- and longer-term maturities for most of that period. The most recent such level represents the lowest since the early '80s.

In announcing that decision, in the context of the quarterly press conference unveiling its broader financing plans, the Treasury went at great lengths to emphasize that the project of lengthening the average maturity of its debt would be implemented very gradually to avoid disrupting market expectations and breaking abruptly with past patterns. Still, a target of reaching an average of 60 months in fiscal 2010 was stated, with an eye on extending it to 84 months over the medium-term, which would represent a historical high.

The Treasury's decision to extend the average maturity of its debt is a sound one, not only on the grounds of prudent borrowing management by spreading out its debt burden over a longer horizon but also on the count of reducing its borrowing costs over time. The latter rationale has generally been a sensitive issue for the Treasury over the years, as it has always maintained that it is not in the business of attempting to "time the market" by adopting views on the future direction of interest rates- an overall sensible approach for a government.

Still, taking advantage, in a measured way, of the unusually low levels of long-term yields (courtesy of a severe financial crisis and associated economic recession) to implement a solid debt management principle of better balancing the ratio of short- to long-term outstanding debt makes perfect sense. Inasmuch as the Treasury wants, understandably, to stay clear of the hazardous enterprise of predicting interest rates, ignoring completely a historical opportunity that would allow it to materially reduce its interest costs on a mushrooming debt over the medium-term would be almost tantamount to malpractice.

Anthony Karydakis

In announcing that decision, in the context of the quarterly press conference unveiling its broader financing plans, the Treasury went at great lengths to emphasize that the project of lengthening the average maturity of its debt would be implemented very gradually to avoid disrupting market expectations and breaking abruptly with past patterns. Still, a target of reaching an average of 60 months in fiscal 2010 was stated, with an eye on extending it to 84 months over the medium-term, which would represent a historical high.

The Treasury's decision to extend the average maturity of its debt is a sound one, not only on the grounds of prudent borrowing management by spreading out its debt burden over a longer horizon but also on the count of reducing its borrowing costs over time. The latter rationale has generally been a sensitive issue for the Treasury over the years, as it has always maintained that it is not in the business of attempting to "time the market" by adopting views on the future direction of interest rates- an overall sensible approach for a government.

Still, taking advantage, in a measured way, of the unusually low levels of long-term yields (courtesy of a severe financial crisis and associated economic recession) to implement a solid debt management principle of better balancing the ratio of short- to long-term outstanding debt makes perfect sense. Inasmuch as the Treasury wants, understandably, to stay clear of the hazardous enterprise of predicting interest rates, ignoring completely a historical opportunity that would allow it to materially reduce its interest costs on a mushrooming debt over the medium-term would be almost tantamount to malpractice.

Anthony Karydakis

Thursday, December 17, 2009

The Undervalued Yuan: And Then There Was Silence

In the early part of the decade, it was a routine occurrence for both U.S. administration officials and politicians in Congress to criticize China's longstanding practice of keeping its currency undervalued by way of pegging it to the dollar. In July 2005, China officially de-linked the yuan from the dollar and let it appreciate by about 20% in the next three years to about 6.83 from approximately 8.3 previously. Still, since July 2008, the yuan has, for all intents and purposes, been tied to the dollar again and remained steady around 6.83. As the dollar has lost approximately 10% of its value on a trade-weighted basis since early March of this year, the yuan has also loyally followed the dollar in its slide.

Still, these days, no loud voices are raised among U.S. officials about the overt manipulation of the currency of a country that continues to run a massive trade surplus. In fact, Congress seems to have decidedly backtracked from its drive of a few years ago to put pressure on the Administration to brand China as a currency manipulator. Instead, it appears that it is increasingly the Europeans that are now taking the lead in putting pressure on China to let the yuan appreciate in accordance with its strong underlying fundamentals.

In a trip to Beijing earlier this month, a group of senior EU officials, which included the ECB President, made strongly the case to the Chinese leadership that it is beneficial for both China and the rest of the global economy to let the yuan strengthen. That was the second time in the last two years that EU officials have tried, publicly- and, presumably, in private as well- to exert pressure on China's top leadership to allow for a more realistic realignment of the yuan vis-a-vis other major currencies.

The euro area's concern over the strengthening of its own currency against the U.S. dollar this year has been frequently, and unmistakably, communicated by the ECB President in the last couple of months, as it has been identified as a headwind for the region's fledgling economic recovery. The fact that the euro is at the same time strengthening by a proportionate amount against the yuan as well, obviously compounds those concerns.

The issue for the euro zone's uneasiness over the undervalued yuan in this phase of the cycle is probably less driven by the more narrow issue of the loss of price competitiveness of its exports to China itself, as its trade volume with that country represents only a modest percentage of the region's total exports. Moreover, the euro area's combined export sector is only about 15% of the total GDP of the 16 countries involved, which suggests that, inasmuch as it would certainly be beneficial for the euro area's tenuous recovery to get the most contribution from every possible component of its GDP, exports will probably not be the defining force for the prospects of that recovery.

The true reasons for Europe's anxiety over the strengthening of the euro against both the dollar and the yuan are related to concerns that a) a period of prolonged strength of the first may undermine the long-term competitiveness of the euro-zone's export-oriented manufacturing sector, which represents close to 20% of its total output, and, b) it may hurt somewhat disproportionately the prospects of Germany's economic recovery in particular, given that country's heavy reliance on exports (accounting for close to half of its GDP, including exports to other euro-zone countries). Germany is of course the pivotal economy for the entire euro area.

In comparing the silence of the U.S. recently toward the artificially undervalued yuan, one cannot avoid thinking that the growing dependence on the Chinese as a major investor in U.S. Treasury securities in an environment of skyrocketing budget deficits has been a factor in taming such voices of protest. This willingness to cultivate a close relationship with a reliable creditor-nation was evident earlier in the year when China's leaders requested assurances from the U.S. President that the country's debt will not be downgraded in view of the massive new issuance of securities; not too long afterwards, Obama did oblige, offering such reassurances in public.

While it is true that the sheer size of China's foreign official reserves also leave that country with few good alternatives to the U.S. Treasury market (which offers a unique degree of liquidity and depth that are of critical importance to any major investor on such scale), it is also true that it would be a particularly destabilizing development that could roil global investors and the U.S. Treasury securities market specifically, to see the two countries relations becoming strained in public over any overt criticism of China's currency manipulation practices.

It is undoubtedly that same need to sustain a seemingly cooperative and fairly harmonious relationship with China on the economic front that has also led the U.S. in recent years scale back dramatically, to the point of non-existence, its previous repeated criticism of that country's human rights record. Not much is heard these days about that either and it is not because of any signficant improvement of that record in the last few years..

At the same time, the Europeans, that are not particularly prone to grandstanding on human rights rhetoric around the world (preferring, instead, to adopt more pragmatic positions and solutions) and are also free of any dependence on China's debt financing prowess, now seem to be the only ones with room to continue pressuring the Chinese on the thorny issue of the undervalued yuan.

Anthony Karydakis

Tuesday, December 15, 2009

A certain Senator from Connecticut

It is hard to turn on the TV or pick up a somewhat legitimate newspaper in the last 48 hours without coming face-to-face with the vaguely sinister grin of a certain Senator from Connecticut, who is at the epicenter of the entire health care reform bill under debate in Congress. The grin is of the "I know I hold all the cards and with a snap of my fingers I can decide whether the whole health care agenda lives or dies" kind.

This Senator is an unsuccessful Vice Presidential candidate in 2000, a miserably failed presidential candidate in 2004, and a defeated candidate in the primary contest of the Democratic party for re-election in the Senate in 2006. An experienced psychologist would be inclined to meticulously trace the origins of that grin to a massive pent-up resentment from all of these three races over the last nine years.

That grin, and its associated hard-nosed obstructionist and uncompromising attitude, is also linked to the fact that he also happens to be the second largest recipient of insurance industry contributions, having received more than 1 million dollars since 1998, according to today's New York Times. Resentment plus the serious need to earn his pay from the "all-too-kind" to him insurance lobby make for a potent motivation to drive a mean, "I now take my revenge on everyone who has repudiated me over the years" type of bargain with the Democratic majority in the Senate.

But, this particular Senator does actually have the whole world at his feet right now and he relishes that immensely. He holds even the current version of a watered-down, meek health care reform project, hostage to his whims.

It is not a classic reflection of the sad state of politics in this country.

It is simply sad.

Anthony Karydakis

Sunday, December 13, 2009

As Lending Continues to Shrink...

Bank lending continued to decline in the most recent period for which data are available, that is the July to September quarter. Loan balances were off by 3%, which represents the biggest quarterly decline since such data started being reported in 1984. Large banks, which have been the primary recipients of the bailout funds, accounted for 75% of that decline.

This is hardly surprising, in view of extensive anecdotal evidence and repeated qualitative assessments of credit conditions by the FOMC in its most recent statements as "tight". Still, there are a couple of intriguing points that spring out of this continuing trend.

1) Until earlier in the year, with the economy marred in a debilitating recession and with both household as well as capital spending in a major retreat, it was hard to disentangle the degree to which the distinctly weak lending patterns reflected the dire state of the banking system from the naturally weak demand for lending during such a period. But with personal spending rising by healthy 2.9% annual rate in Q3 and private fixed investment turning modestly positive (capital spending itself was off again- albeit by the smallest amount since Q2 2008), it is now clear that the significant turnaround of economic conditions in Q3 was not associated with an increased willingness of banks to lend more. In other words, the reluctance of banks to lend remains deeply entrenched even in the face of a presumed improvement in the demand for credit.

2) The above suggests that the sharp pick-up in consumer spending is being financed either by the increased in household wealth resulting from the stock market rally or by a decrease in the savings rate. Although the latter was not evident yet in the October data (the rate was off only by an inconsequential 0.2% to 4.4% in that month, which represents the most recently reported figure for that series), a strong likelihood exists that the improvement in personal consumption will be increasingly relying on a decline in the saving rate.

This would shatter the expectations in some quarters that the traumatic experience of the latest recession may be leading to a new paradigm in the U.S. economy, where consumers save a higher percentage of their current income. With bank lending activity unlikely to return to normal levels for some time, employment and income growth on track for only a gradual pace improvement ahead, and pent-up household demand waiting to be fullfilled, a downtrend in the saving rate over the next 9 to 12 months remains a distinct probability.

Anthony Karydakis

Thursday, December 10, 2009

A Propos Greece's Troubles

The precarious shape a number of euro-zone economies have found themselves in recently has dominated financial market headlines in the last few days. Ireland, Spain, and Greece seem to have joined other "second-tier" European countries, like Latvia and Hungary, in experiencing widespread loss of confidence in the quality of their sovereign debt. The draconian measures to address the budget gap that the Irish government announced yesterday have received an initially positive response but uneasiness over their effectiveness remains high.

http://online.wsj.com/article/SB126039835690184387.html

http://online.wsj.com/article/SB10001424052748704825504574586410597112166.html

At the core of the attention-getting developments of the last few days is the massive budget deficits and total amount of debt that these countries have accumulated, mostly, but not exclusively, due to the financial crisis and global economic downturn of the last two years. Although, it is actually unlikely that a euro-zone country, like Greece (which is facing the most serious problems) will be allowed by the EU to default on its debt- with Angela Merkel reminding investors as much earlier today-credit default swaps have soared.

A few thoughts.

a) The reassurance offered by the powers-that-be in the euro-system about offering help to its members currently in trouble is obviously a positive development, but it may not be enough to resolve the issue. Greece is already resisting EU pressure to implement any major belt-tightening measures of its own as politically untenable and offers only promises of bringing its budget deficit from 12.7% of GDP this year to about 10% next year. That is likely to be viewed as a frustratingly slow pace to many. Against such obstinacy, it may not be too far down the line, where massive bets against the country's ability to contain its debt burden start being placed by global macro hedge funds- not totally unlike those that were already pushing Iceland (a non-euro zone country) against the wall as the financial crisis was erupting in 2008. (In fact the second of the above links describes exactly those emerging strategies by some). This would represent a major complication for any bail-out efforts by the EU.

2) Directly linked to the above point, the problems that Greece and Spain are facing- and, possibly, Ireland, Italy, and Portugal to various degrees- are not solely the result of the size of their budget deficits per se but more of the lack of credibility that those countries have in the eyes of global investors in terms of their determination to bring them under control. For example, Germany's budget deficit is surpassing 6% of GDP this year but Germany's sovereign debt still carries some of the lowest rates in the euro area and credit default swaps on such debt have not budged. Nobody questions Germany's commitment to reining in the deficit as economic growth picks up into next year. Of course, another key differentiating factor is the total amount of debt of the various countries involved, with Greece's exceeding 125% of its GDP, while other healthier euro-zone economies are only moderately exceeding the 60% cap mandated by the "growth and stability" pact.

3) In a way, the current predicament of the three main countries in trouble currently represents the moment of reckoning for reckless and short-sighted policies earlier in the decade, mostly driven by a goal of creating an aura of unusual prosperity largely built on sand (Ireland, Greece). The financial crisis and associated economic downturn simply helped expose the underlying fault lines of such growth.

4) Finally, it is tempting to highlight that there has been a reversal of past patterns and prevailing stereotypes as to the resiliency that different economies around the world demonstrate in the face of global financial market events of extreme stress. While emerging market economies used to be considered "high-risk" in such situations- and there is admittedly a long history of defaults on their debt to support that perception- it has been exactly those economies that have weathered best the financial turmoil of the last two years. Even Argentina, a serial offender in terms of defaulting on its debt in the last 30 years, is taking positive steps opening up its access to international capital markets again, by announcing today a decision to swap out of $20 billion of defaulted debt.

http://online.wsj.com/article/SB126039835690184387.html

http://online.wsj.com/article/SB10001424052748704825504574586410597112166.html

At the core of the attention-getting developments of the last few days is the massive budget deficits and total amount of debt that these countries have accumulated, mostly, but not exclusively, due to the financial crisis and global economic downturn of the last two years. Although, it is actually unlikely that a euro-zone country, like Greece (which is facing the most serious problems) will be allowed by the EU to default on its debt- with Angela Merkel reminding investors as much earlier today-credit default swaps have soared.

A few thoughts.

a) The reassurance offered by the powers-that-be in the euro-system about offering help to its members currently in trouble is obviously a positive development, but it may not be enough to resolve the issue. Greece is already resisting EU pressure to implement any major belt-tightening measures of its own as politically untenable and offers only promises of bringing its budget deficit from 12.7% of GDP this year to about 10% next year. That is likely to be viewed as a frustratingly slow pace to many. Against such obstinacy, it may not be too far down the line, where massive bets against the country's ability to contain its debt burden start being placed by global macro hedge funds- not totally unlike those that were already pushing Iceland (a non-euro zone country) against the wall as the financial crisis was erupting in 2008. (In fact the second of the above links describes exactly those emerging strategies by some). This would represent a major complication for any bail-out efforts by the EU.

2) Directly linked to the above point, the problems that Greece and Spain are facing- and, possibly, Ireland, Italy, and Portugal to various degrees- are not solely the result of the size of their budget deficits per se but more of the lack of credibility that those countries have in the eyes of global investors in terms of their determination to bring them under control. For example, Germany's budget deficit is surpassing 6% of GDP this year but Germany's sovereign debt still carries some of the lowest rates in the euro area and credit default swaps on such debt have not budged. Nobody questions Germany's commitment to reining in the deficit as economic growth picks up into next year. Of course, another key differentiating factor is the total amount of debt of the various countries involved, with Greece's exceeding 125% of its GDP, while other healthier euro-zone economies are only moderately exceeding the 60% cap mandated by the "growth and stability" pact.

3) In a way, the current predicament of the three main countries in trouble currently represents the moment of reckoning for reckless and short-sighted policies earlier in the decade, mostly driven by a goal of creating an aura of unusual prosperity largely built on sand (Ireland, Greece). The financial crisis and associated economic downturn simply helped expose the underlying fault lines of such growth.

4) Finally, it is tempting to highlight that there has been a reversal of past patterns and prevailing stereotypes as to the resiliency that different economies around the world demonstrate in the face of global financial market events of extreme stress. While emerging market economies used to be considered "high-risk" in such situations- and there is admittedly a long history of defaults on their debt to support that perception- it has been exactly those economies that have weathered best the financial turmoil of the last two years. Even Argentina, a serial offender in terms of defaulting on its debt in the last 30 years, is taking positive steps opening up its access to international capital markets again, by announcing today a decision to swap out of $20 billion of defaulted debt.

It is now, countries in the heart of Europe that are facing a particularly bleak predicament that represents a significant challenge for the cohesiveness of the euro system and testing the limits of patience of global investors.

All in all, another strong reminder, following Dubai's recent problems, that, although the global financial crisis has been by and large successfully contained, pockets of extreme fragility have been left behind and are not likely to disappear any time soon.

Anthony Karydakis

All in all, another strong reminder, following Dubai's recent problems, that, although the global financial crisis has been by and large successfully contained, pockets of extreme fragility have been left behind and are not likely to disappear any time soon.

Anthony Karydakis

Tuesday, December 8, 2009

No Deflation Ahead

A number of influential, and legitimate, voices- including the Fed Chairman and PIMCO- have been raised recently to the effect that they expect the pace of the U.S. economic recovery to be a very moderate one. Although, the term "moderate" is a qualitative one and is probably used by Bernanke and PIMCO having different numbers attached to it, most of those who subscribe to that view are also calling for inflation to continue drifting lower over the next year or two, with some actually raising the specter of deflation as a result (see also a previous post titled "PIMCO's Bet").

Given that inflation is a lagging indicator and there is a considerable amount of inertia associated with its behavior, anticipating a further downward drift in the pace of price increases over the next year (particularly in regards to core inflation) is reasonable; promoting the view though that deflation is a plausible risk in the context of an unfolding expansionary period begs some further explanation.

Irrespective of such diverse views on the price outlook however, a down-to-the-earth look at some key measures of inflation expectations reveals an entirely different view.

After collapsing in the fall of 2008, overwhelmed by pervasive fears of a banking system disaster and a major, depression-like, economic downturn, TIPS break-evens (the spread between nominal Treasury yields and the yield on Treasury inflation-protection securities, which implies the expected rate of inflation over the investment period) have been widening steadily since the beginning of the year. This reflects underlying expectations that the overall CPI is likely to be returning to its recent historical averages of about 2%-2.5%, in the years ahead. In fact, both the 5- and 10-year break-evens currently stand very close to their levels prior to the Lehman episode in September 2008 (see below).

5-year TIPS Break-evens

Source: Bloomberg

10-year TIPS Break-evens

Source: Bloomberg

Simply put, the restoration of these spreads to pre-crisis levels, reflects the belief that the worst of the banking crisis is behind us and that the economy is recovering at a sufficient pace (irrespective of what specific number, or additional qualitative adjective, is attached to it) to ensure the gradual return of inflation to trend. As one would have expected the implied rate of inflation expectations over the 5-year horizon is somewhat lower than the one over the 10-year horizon, as the weight of 2010 (when inflation should remain especially weak) is obviously greater in a 5-year period as opposed to a 10-year one.

Another, fairly closely watched but admittedly "soft", gauge of inflation expectations is the "5- to 10-year inflation expectations" component of the University of Michigan Consumer Sentiment Survey, which continues to hover around the 3% mark in recent months. This is somewhat higher than the anticipated rate of inflation reflected in the TIPS break-evens, which is to be expected, as consumers' perception of inflation is typically associated with a higher number than the one officially measured by the CPI. On that score, it is worth recognizing that even the "short-tern inflation expectations" component of the University of Michigan survey (representing a 1-year horizon) is also anchored just below 3%.

Somewhat unscientific as these consumer inflation expectations measures may be, they still corroborate the financial market's fairly more rigorous perceptions of the price outlook and they certainly betray no uneasiness over any prospect of deflation, which, at the margin, could make the latter a self-fulfilling prophecy of sorts.

Deflation, as a trend and not as a short-lived quirk of year-on-year comparison in the various price statistics, is a phenomenon very hard to come by and Japan is the only major industrialized country to have experienced it in recent history- largely as a result of a double meltdown in its stock markets and banking system in the 90s and a notoriously slow policy response to address it. But both of these two potentially extremely destabilizing dynamics seem to have been contained in the U.S. at the present and, as a result, have convincingly pushed the risk of deflation to the sidelines.

5-year TIPS Break-evens

Source: Bloomberg

10-year TIPS Break-evens

Source: Bloomberg

Simply put, the restoration of these spreads to pre-crisis levels, reflects the belief that the worst of the banking crisis is behind us and that the economy is recovering at a sufficient pace (irrespective of what specific number, or additional qualitative adjective, is attached to it) to ensure the gradual return of inflation to trend. As one would have expected the implied rate of inflation expectations over the 5-year horizon is somewhat lower than the one over the 10-year horizon, as the weight of 2010 (when inflation should remain especially weak) is obviously greater in a 5-year period as opposed to a 10-year one.

Another, fairly closely watched but admittedly "soft", gauge of inflation expectations is the "5- to 10-year inflation expectations" component of the University of Michigan Consumer Sentiment Survey, which continues to hover around the 3% mark in recent months. This is somewhat higher than the anticipated rate of inflation reflected in the TIPS break-evens, which is to be expected, as consumers' perception of inflation is typically associated with a higher number than the one officially measured by the CPI. On that score, it is worth recognizing that even the "short-tern inflation expectations" component of the University of Michigan survey (representing a 1-year horizon) is also anchored just below 3%.

Somewhat unscientific as these consumer inflation expectations measures may be, they still corroborate the financial market's fairly more rigorous perceptions of the price outlook and they certainly betray no uneasiness over any prospect of deflation, which, at the margin, could make the latter a self-fulfilling prophecy of sorts.

Deflation, as a trend and not as a short-lived quirk of year-on-year comparison in the various price statistics, is a phenomenon very hard to come by and Japan is the only major industrialized country to have experienced it in recent history- largely as a result of a double meltdown in its stock markets and banking system in the 90s and a notoriously slow policy response to address it. But both of these two potentially extremely destabilizing dynamics seem to have been contained in the U.S. at the present and, as a result, have convincingly pushed the risk of deflation to the sidelines.

Further disinflation is a plausible outcome in the foreseeable future, but much to the likely disappointment of the merchants of doom, deflation is not.

Anthony Karydakis

Anthony Karydakis

Friday, December 4, 2009

The Employment Picture Brightens Up Suddenly, In a Major Way

Labor market conditions continue to improve at a fast clip and the November employment report provided strong confirmation of that trend. This conclusion is not based on the decline in the unemployment rate to 10.0% from 10.2% (a nearly inevitable correction from a curiously sharp jump of the rate in October) but on a consistent message from just about every major aspect of the data.

It is not only that November's decline in payrolls was a mere 11,000 but, even perhaps even more importantly, there was a massive net cumulative upward revision of 159,000 in the payroll data for the prior two months. The result is a dramatically different profile of recent payroll trends, showing a faster improvement than previously thought. Payroll declines in the last 3 months have averaged 87,000 a month versus average declines of 307,000 in the preceding 3-month period and -491,000 in the 3-month period prior to that.

Source: Bureau of Labor Statistics

Adding impetus to the impressive strength of the report- compared to the relatively recent past- the average workweek rose to 33.2 hours from its cycle-low of 33.0 hours. Any moderate sustained rise in the workweek is usually viewed as a precursor of more hiring down the line, as there are limits as to how intensively employers can utilize their existing labor force before adding to it. The manufacturing workweek also jumped by 0.3 hours to 40.4, supporting evidence of a significant turnaround in that sector, as manifested by the ISM and other manufacturing surveys in recent months.

Both construction and manufacturing employment fell last month, by 27,000 and 41,000 respectively, but these are two sectors unlikely to become significant sources of job creation in the foreseeable future, as construction is likely to remain in deep freeze for some time and the bulk of increased output in manufacturing recently comes from a rise in productivity. It is also a sign of the ongoing caution that employers are still exercising in terms of hiring that temporary jobs rose by 57,000 in November and have increased by a total 117,000 since July.

However, all of the still present pockets of weakness in the payroll data need to be understood in the context of the dynamic that prevails around turning points of the cycle- meaning that not all sectors will be showing the same measure of improvement simultaneously and this is likely to be particularly true this time in view of the severity of the last recession and the major dislocations it has caused.

With the pace of layoffs slowing precipitously in the last several weeks, as measured by a strong downtrend in initial unemployment claims, monthly payroll data are poised to start turning positive in the coming months. In fact, the most reasonable expectation at this point is that by early next year, we will start seeing modest to moderate monthly gains, while the unemployment rate may continue to linger around its cycle-highs. But today's report, along with the totality of the other pieces of economic data recently, suggests that the impetus that this economic recovery is having may have been seriously underestimated.

Anthony Karydakis

It is not only that November's decline in payrolls was a mere 11,000 but, even perhaps even more importantly, there was a massive net cumulative upward revision of 159,000 in the payroll data for the prior two months. The result is a dramatically different profile of recent payroll trends, showing a faster improvement than previously thought. Payroll declines in the last 3 months have averaged 87,000 a month versus average declines of 307,000 in the preceding 3-month period and -491,000 in the 3-month period prior to that.

Source: Bureau of Labor Statistics

Adding impetus to the impressive strength of the report- compared to the relatively recent past- the average workweek rose to 33.2 hours from its cycle-low of 33.0 hours. Any moderate sustained rise in the workweek is usually viewed as a precursor of more hiring down the line, as there are limits as to how intensively employers can utilize their existing labor force before adding to it. The manufacturing workweek also jumped by 0.3 hours to 40.4, supporting evidence of a significant turnaround in that sector, as manifested by the ISM and other manufacturing surveys in recent months.

Both construction and manufacturing employment fell last month, by 27,000 and 41,000 respectively, but these are two sectors unlikely to become significant sources of job creation in the foreseeable future, as construction is likely to remain in deep freeze for some time and the bulk of increased output in manufacturing recently comes from a rise in productivity. It is also a sign of the ongoing caution that employers are still exercising in terms of hiring that temporary jobs rose by 57,000 in November and have increased by a total 117,000 since July.

However, all of the still present pockets of weakness in the payroll data need to be understood in the context of the dynamic that prevails around turning points of the cycle- meaning that not all sectors will be showing the same measure of improvement simultaneously and this is likely to be particularly true this time in view of the severity of the last recession and the major dislocations it has caused.

With the pace of layoffs slowing precipitously in the last several weeks, as measured by a strong downtrend in initial unemployment claims, monthly payroll data are poised to start turning positive in the coming months. In fact, the most reasonable expectation at this point is that by early next year, we will start seeing modest to moderate monthly gains, while the unemployment rate may continue to linger around its cycle-highs. But today's report, along with the totality of the other pieces of economic data recently, suggests that the impetus that this economic recovery is having may have been seriously underestimated.

Anthony Karydakis

Wednesday, December 2, 2009

In Praise of the Bernanke Fed

(Fair warning: This is a long article. It requires more than 20 seconds to read it!)

It certainly feels as if the favorite game among members of Congress these days is to outbid each other in trying to limit the various aspects of the Fed's powers and independence. The underlying reason is both transparent and cynical, all blended with a strong hint of ignorance.

Playing the populist card in attempting to show how outraged they are too by Wall Street's bailout in the midst of the financial crisis, while Main Street was left holding the bag (also known, as the bailout cost), people in Congress are focusing their criticism on the Fed. Such criticism has flared up in recent days, with Bernanke's own confirmation hearings underway and various bills designed to overhaul the bank regulatory framework making their way through Congressional committees.

That rising level of attacks on the Fed, and the implied threat to its regulatory and monetary policymaking authority, prompted the Fed Chairman to write an article in The Washington Post this past weekend, offering a spirited defense of the Fed's independence and crucial leadership role that it should continue to play in the context of any regulatory overhaul.

The main arguments of those who cannot criticize the Fed quickly enough are three:

a) The Fed, as a bank regulator and supervisor, did a very poor job at recognizing the steadily growing risks to the financial system that led up to its near-meltdown following Lehman's demise.

b) The Fed was at the forefront of the drive to bailout the major financial institutions once the crisis erupted, although it was precisely those same institutions that, by way of their reckless and dubious behavior, were responsible for the financial crisis itself.

c) It is unacceptable in a "democratic society" for the Fed to have so much power and independence from both the executive and legislative branches of the government; therefore, it needs to be brought under more supervision and some of its powers to be taken away.

The first of the above points can be disposed of fairly easily, by admitting that indeed the Fed did a miserable job at identifying the build-up to the financial crisis and had shown little interest in trying to rein in the tremendous proliferation of exotic derivative instruments for the most part of the decade. Although the bulk of of this failure should -out of fairness- be assigned to Greenspan's irrepressibly free-market, hands-off, philosophy, there is no dispute over the Fed's, as an institution, embarrassing failure here. Bernanke plainly acknowledges this in his article and highlights a number of concrete measures the Fed has taken recently to prevent such an enormous lapse again in the future, like beefing up bank examiners' teams, tightening the supervision practices etc. One can raise questions as to how effective these measures will be in correcting the problem but there is little reason to believe that another regulator would, for some unexplained reason, be more nimble and effective in dealing with such problems.

The second of the above points is where a giant misconception and a good dose of hypocrisy by the Fed's Congressional critics merge. The bailout of "Wall Street" was not an elective action but borne out of necessity to prevent the collapse of the entire financial system, which would have had unspeakable consequences for Congress's favorite constituency- the "Main Street". As Bernanke had pointed out at one point during the heady days of the crisis, you don't let a whole neighborhood burn down to punish the arsonist who may live in that neighborhood himself; you first put out the fire any way you can and then try to deal with the arsonist.

The whole idea that, somehow, the major financial institutions should have been allowed to collapse because we didn't want to burden the Main Street with the cost of keeping them alive enters squarely into the sphere of absurd. Someone in Congress should perhaps find the time, and courage, to explain to that famous "average American on the street" that this is the way the capitalist system that they all learn to worship from kindergarten on really works. It is based on the unspoken pact that when the financial industry does well, those that are part of it get obscenely compensated for their spirit of "entrepreneurship" and "willingness to take risk". Rewarding success is the ultimate value in the society and no one is complaining.

But, when the industry suffers a life-threatening heart attack (irrespective of whether it is due to its own fault or that of others), and threatens to plunge the economy and global financial system into an abyss, the only available course of action is to frantically try to resuscitate it at all costs. And, given the close symbiotic relationship that Congress, the Executive branch, and corporations enjoy in the brand of unfettered capitalism in this country, the cost of salvaging the financial system will naturally need to be borne by those who can be forced to do so- that is the Main Street. It is a pity, and arguably a high point of hypocrisy, that no one has explained to the "average person on the street" how the true free-market system is really meant to work- not on paper, but in reality. Otherwise, extensive government intervention to meaningfully rein in the systemically dangerous greed of the system is quickly labeled as "socialism" which, again, in the eyes of the Main Street is probably far more abhorrent than Wall Street.

On that last seemingly unfair issue, the Bernanke Fed has actually been at the forefront of supporting a provision in the proposed overhaul of the regulatory system, according to which all major financial institutions will be required to pay a premium to a special fund to cover the cosy of any such bailouts in the future. An innovative and sensible idea, although its final version, if enacted at all, will probably be watered down appreciably. But, at least, the Fed is showing tangible signs that they are drawing some sensible conclusions from the crisis.

And, then, there is the paramount issue that those who savage the Fed's role in the recent banking crisis either ignore or are simply unable to appreciate.

The Fed's response to the crisis was phenomenally aggressive, imaginative, and, ultimately, effective in preserving the financial system's integrity. They invented an array of new tools on the fly to combat the crisis, they turned traditional monetary policymaking at times on its head, they assumed some major risks. The Bernanke Fed's response to the events of the post-Lehman period will probably be studied at all major Business Schools around the country (and beyond) 30, 40 years, or more, from now. The determination and swiftness that the Fed showed during that period have already become part of the global finance's history books. It is ironic that against that backdrop some of the nation's elected representatives now profess outrage by the Fed's role in the financial crisis. Ignorance can be their best excuse, but still...

As for the third argument used by Bernanke's critics, that the Fed is too unaccountable for the amount of power that it wields within the entire financial system, that "power" needs to be broken down into its two key components:

On the count of conducting monetary policy independently, it would require an enormous amount of bad faith to argue that it is best to subject such decisions to direct influence by either the executive or the legislative branches of the government and bring them under the control of people that would give priority to short-term political expediency objectives rather than the Fed's long-term goals of sustainable economic growth and price stability. On the count of the Fed's becoming more transparent in the way it operates, this is probably one of the major prevailing misconceptions about the Fed. As Bernanke's article points out, he personally delivers several lengthy Congressional testimonies each year answering questions at great length, the Fed's balance sheet is regularly audited, the Fed provides monthly detailed reports about its various special facilities, and the FOMC always announces in detail its decisions regarding monetary policy. A transparency problem?

Perhaps, it's time for those who do actually have a better understanding than some in Congress of how the Fed operates and what its role exactly was in the recent financial crisis, to stand up and defend the Fed and its independence.

The financial system is still standing today, and Ben Bernanke may be the single most important reason for that.

Anthony Karydakis

Subscribe to:

Comments (Atom)